Crypto Volatility Index (CVI) - How to Long/Short Volatility?

Trading Crypto's Volatility

A Decentralized VIX in Crypto

Many are familiar with VIX, the volatility index measuring the market’s expectations of short-term price fluctuations in the next 30 days.

Crypto also has its decentralized version of VIX called CVI, the crypto volatility index.

CVI was created by the COTI team, in collaboration with the original creator of VIX, Prof. Dan Galai.

The CVI tracks the 30-day implied volatility of bitcoin and Ethereum, ranging between 0-200.

0-85 ≈ Low volatility

85-105 ≈ Medium volatility

105-200 ≈ High volatility

CVI calculates this number by pulling inputs directly from Deribit exchange, crypto’s largest CEX for derivatives and options, and other platforms like CBOE.

It is done through Chainlink oracles and external adapters. All calculations and aggregations are done off-chain before pushing the final output on-chain as a single value for the CVI.

At regular intervals, the Chainlink oracle nodes would fetch market data from the options platforms and reference back with the previous value to see if it needs to be updated.

Volatility Token - CVOL

The token that tracks the CVI is CVOL. By longing/shorting CVOL, you are trading the CVI.

CVOL token is decentralized, permissionless, and can be traded 24/7.

The protocol has been around since 2021, and they recently launched v3, which aims to target liquidity and scalability issues.

Since the volatility index is a mean reverting asset and ranges between 0-200. Time decay has to be incorporated into the design.

Otherwise, someone could buy or mint low and hold indefinitely until it reverts to the mean to sell and earn a risk-free profit.

In options terms, this is known as “Theta,” which measures the rate of decline in value as time passes.

CVI charges a decay fee and is exposed to Theta. So it’s something to be held only in the short term. Assuming all things equal, the CVOL token’s value would decrease as time passes.

This creates three problems.

CVOL would lose peg to the CVI over time

LPs would not want to provide liquidity for the long term for an asset that declines in value over time.

Demand for CVOL can’t scale up if there is no liquidity

Overview of CVI v3 Platform - Theta Vault

The solution is a new “Theta Vault” in v3, launched in Nov 2022.

Theta Vault will be the only gateway liquidity source for any LPs who want to provide liquidity and take the counterparty trade of traders.

USDC would be deposited as collateral and algorithmically distributed to two different liquidity avenues for longs:

The CVI Platform (primary market for minting/burning)

The DEX (secondary market for buying/selling)

The maximum profits for longs will be the supply of CVOL tokens held by longs multiplied by the max CVI (200).

When traders close out their position and burn CVOL tokens, liquidity is guaranteed from the Theta Vault, and the losses will be on the LP.

As for the DEX on the secondary market, it is a CVOL-USDC liquidity pair on Sushi Arbitrum, but a concentrated liquidity pair is coming soon on Polygon.

If the price on the CVI platform is = trading price on DEX, Theta Vault may add additional liquidity into the DEX, or else there will be an arbitrage opportunity.

How does CVOL maintain its peg to the CVI (Arbitrage + Rebasing)

There is a twin-engine to keep the CVOL closely pegged to the CVI. One is arbitrage, and the other is rebasing.

For arbitrage, the price of the CVOL token is compared on the primary platform (CVI platform) and the secondary market DEX (Sushiswap).

The CVI platform is the primary market and takes reference directly from the CVI source. The price on the DEX is controlled by the markets and attempts to follow the platform price through arbitraging.

If the platform price is higher than the DEX price, arbitragers would buy from the DEX and sell it at a premium on the CVI platform to earn more USDC. The price on DEX goes up to reflect the platform price as a result.

Conversely, if CVI drops, the platform price is lower than the DEX price, arbitragers would mint from the CVI platform and sell them on the DEX to earn more USDC. More sellers on DEX = CVOL price on DEX drops to reflect the CVI change.

Since Theta Vault controls both the primary and secondary markets, all arbitrage fees and funding fees go back to the Vault, and those who provide liquidity will not be exposed to any Theta loss from time decay.

By providing liquidity into the Theta Vault, you earn from

Funding fees paid by longs

Swap fees

Mint/Arbitrage fees

Traders’ net profits/losses (could be a loss if they are winning, same as GLP)

The other engine is rebasing.

If there is no rebasing, the intrinsic value of CVOL would drop and move further away from the CVI due to the time decay funding fees.

Arbitragers would come in and mint more CVOL tokens to sell on the DEX, making the price drop even further.

In rebasing, the protocol will reduce the quantity supply of the CVOL tokens and increase the price, but the USD value remains the same (after adjusting for funding fees).

The target reference value used in the rebasing will be the CVI index.

This way, the CVOL price on the DEX can stay tight to the CVI index yet account for funding fees by adjusting lower quantity supply.

The rebasing helps peg CVOL to CVI, while arbitrage helps to maintain price equilibrium on the DEX and the CVI platform.

Through the twin-engine mechanism, it resolves the CVOL pegging and the time decay issue.

Long Volatility

From a user perspective, if you want to long volatility, you can

Buy the CVOL tokens on the secondary market DEX, or

Mint CVOL tokens by depositing USDC as collateral on the CVI platform.

Minting CVOL tokens directly has no price impact or slippage, but you have to wait about 60 minutes before you receive the CVOL tokens.

Buying directly on DEX has regular slippage and price impact differences, but you receive the token immediately.

The CVOL tokens would automatically rebase themselves (quantity decreases every day) to reflect the funding fees paid.

Crypto is volatile, and CVOL is a perfect way to increase your exposure to volatility.

Longing volatility can be profitable for high-impact events like Fed’s FOMC meeting, bankruptcy news, CPI data, etc. You don’t care price goes up or down as long as it is volatile.

Or you could use it as a hedge for your portfolio. For example, if your positions are net long, but you fear the market might get volatile soon, you could buy CVOL, and if it gets volatile, you could profit and reduce your losses.

Finally, you could deploy crab strategies and delta-neutral plays that do well in dull markets earning yields, but you worry about volatility. You could also get CVOL to hedge against the markets if it does not go sideways.

But once again, CVOL is not a buy-and-hold play due to the theta (time decay). It is only effective in periods of expected volatility unless some other protocols can hedge away time decay. But so far, we do not have any doing that yet.

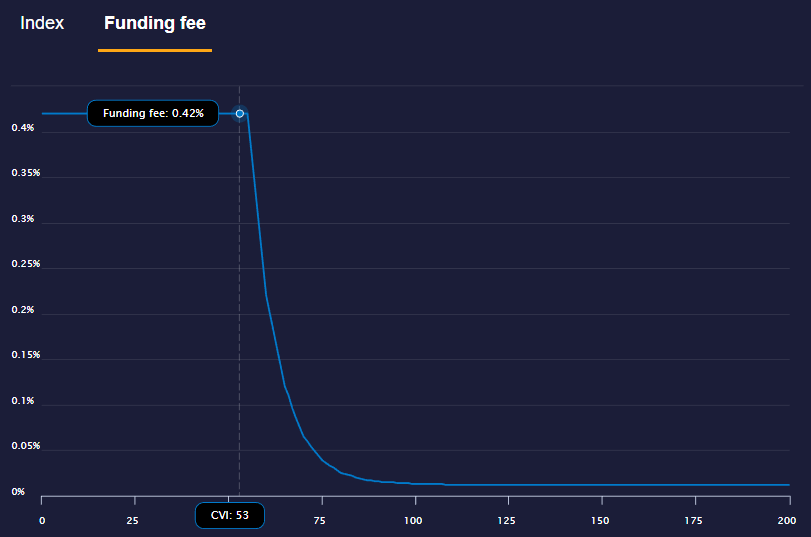

The lower the CVI, the higher the upside potential, but the higher the funding fee you pay hourly to the shorts, the counterparty who provided liquidity in the Theta Vault.

Assuming funding fees are at 0.4% when CVI is ATL, that is equivalent to a 9.6% loss in a day. And in about ten days, your capital will be wiped out, assuming all things equal. So you desperately need CVI to move fast when you are long.

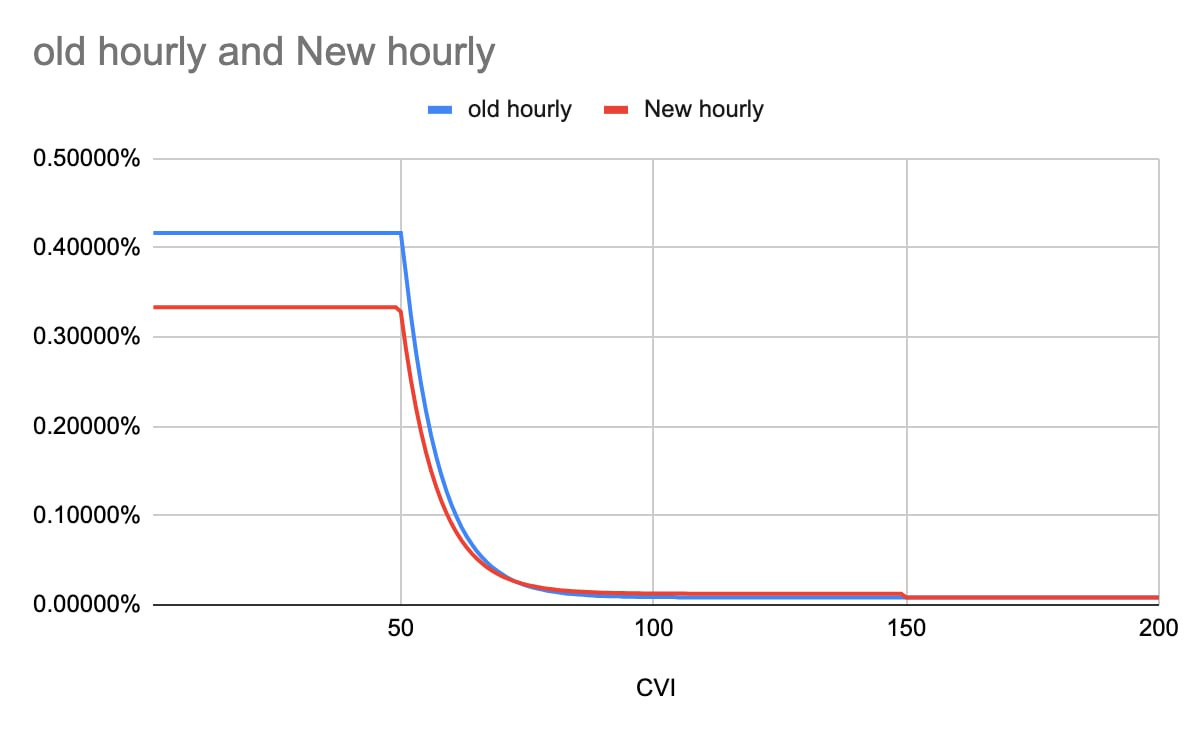

The team is aware of the funding rate issues and has made some temporary adjustments (red line).

Moving forward, the funding rate would be dynamically adjusted based on demand rather than an arbitrary CVI number.

The feature is already ready but has yet to be activated. The idea is to make it attractive enough for buyers to buy and sellers to provide liquidity.

But as of now, the liquidity providers of CVOL are earning high APR yields because the CVI is at an all-time low (higher risk for sellers), and funding fees are ATH. But nothing is risk-free as traders’ profits = your losses in the vault.

There are times when the CVI stays depressed for long periods, though it will always revert to the mean; how fast it reverts determines your profit and loss as a buyer.

Governance - GOVI

The governance token for the platform and protocol is GOVI. There are no VCs, allocation to whales or fundraising. It is a fair launch product.

The Max supply is 32M. Based on Coinmarketcap, about 56% of the supply is in circulation.

53% goes to CVI platform users

15% Development Fund

15% LP Incentives

10% Airdrops

7% GOVI Stakers

Staking GOVI earns 50% of CVOL mint fees and 100% of burn fees. 85% of platform fees generated will be collected and market buyback GOVI tokens.

The tokens would then be re-distributed to the CVI ecosystem, traders, LPs, and stakers.

The team is also revising GOVI tokenomics based on GMX’s model. So, for example, it could have an esGOVI, locking up for multiplier rewards, real yields, etc. The progress is currently in the advanced dev phase.

Some of the recent governance proposals that just passed include:

Reducing GOVI incentives on Uniswap v2 (moving towards zero incentives)

Uniswap v3 concentrated liquidity for CVOL tokens via ICHI Vaults

Product Adoption

About 10,000 CVOL tokens are in circulation, of which 80% are held on the Sushiswap DEX, CVI’s own liquidity from Theta Vault.

That means around 150 addresses hold the remaining 2,000 CVOL tokens.

From a liquidity provider (seller)’s standpoint, the current max drawdown is = 2,000* 200 (CVI max profit) = $400k.

That is about 11% of the $3.6m deposited in the Theta Vault.

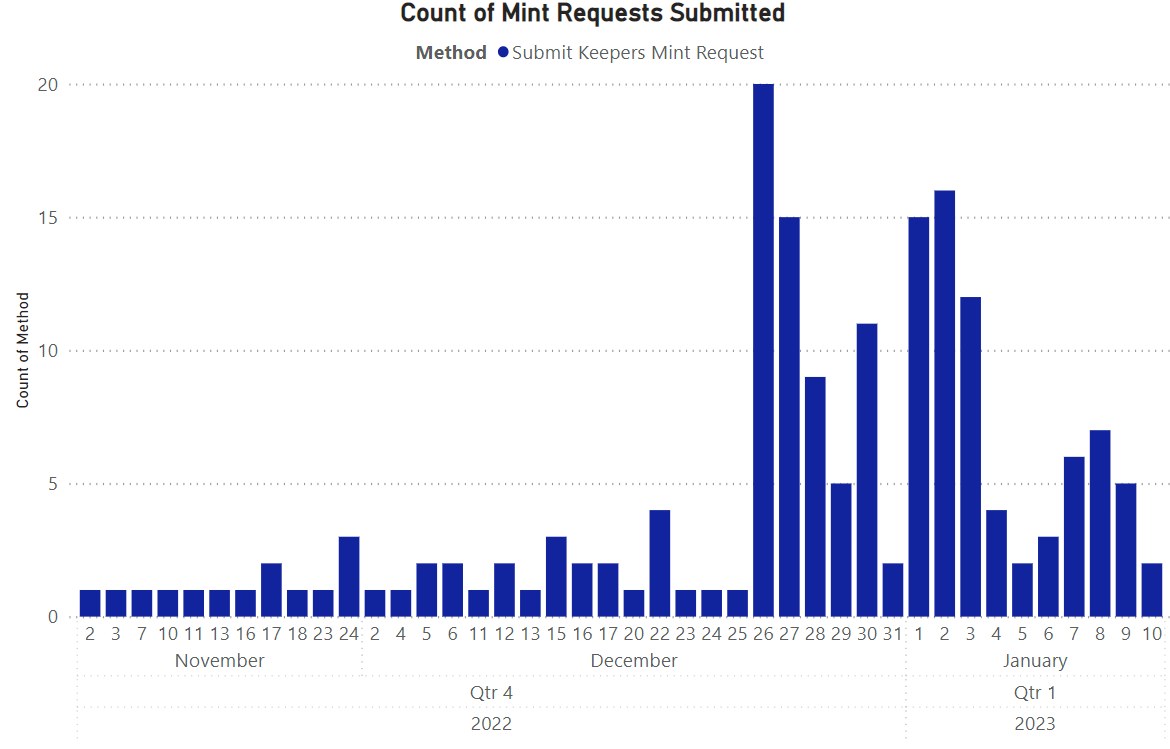

Looking at the count of minting requests on the CVI platform, the adoption is still relatively low. We are still very early, and v3 was only launched in Nov 2022.

But the product is live and working and is slowly gaining traction in Jan 2023.

Looking at the GOVI token, there are only about 3.2k holders.

Smart money is not in yet after the v3 launch, and the FDV is only about $15m~.

When funding fees are reduced, more longs come in, open interest goes up, yields go up, theta vault increases, and the whole flywheel kicks in.

It is foreseeable that other products in the Arbitrum ecosystem might integrate or create derivatives on top of CVOL once the product gain adoption.

Once that happens, we could see a new narrative of volatility trading in crypto.