Introduction to Power Perpetuals

Squeeeethh

1. What are Power Perpetuals?

Power perpetual is a new type of derivative first introduced by the chads at Paradigm.

It is a derivative that basically tracks the power of an underlying asset. (e.g., ETH²)

If the price of ETH doubles, you would only make 2x if you hold spot. But a power perp makes 4x since it is (2 * ETH²)

Power perpetual with a power greater than 1 will have a positive convex function.

This means the more price goes up, the more exponential your returns will be. Imagine all your returns getting “squared.”

And on the flip side, the more the price goes down, the slower the rate of losses.

In options terms, this is called positive gamma which is the “rate of change” of the returns for each dollar change in the asset.

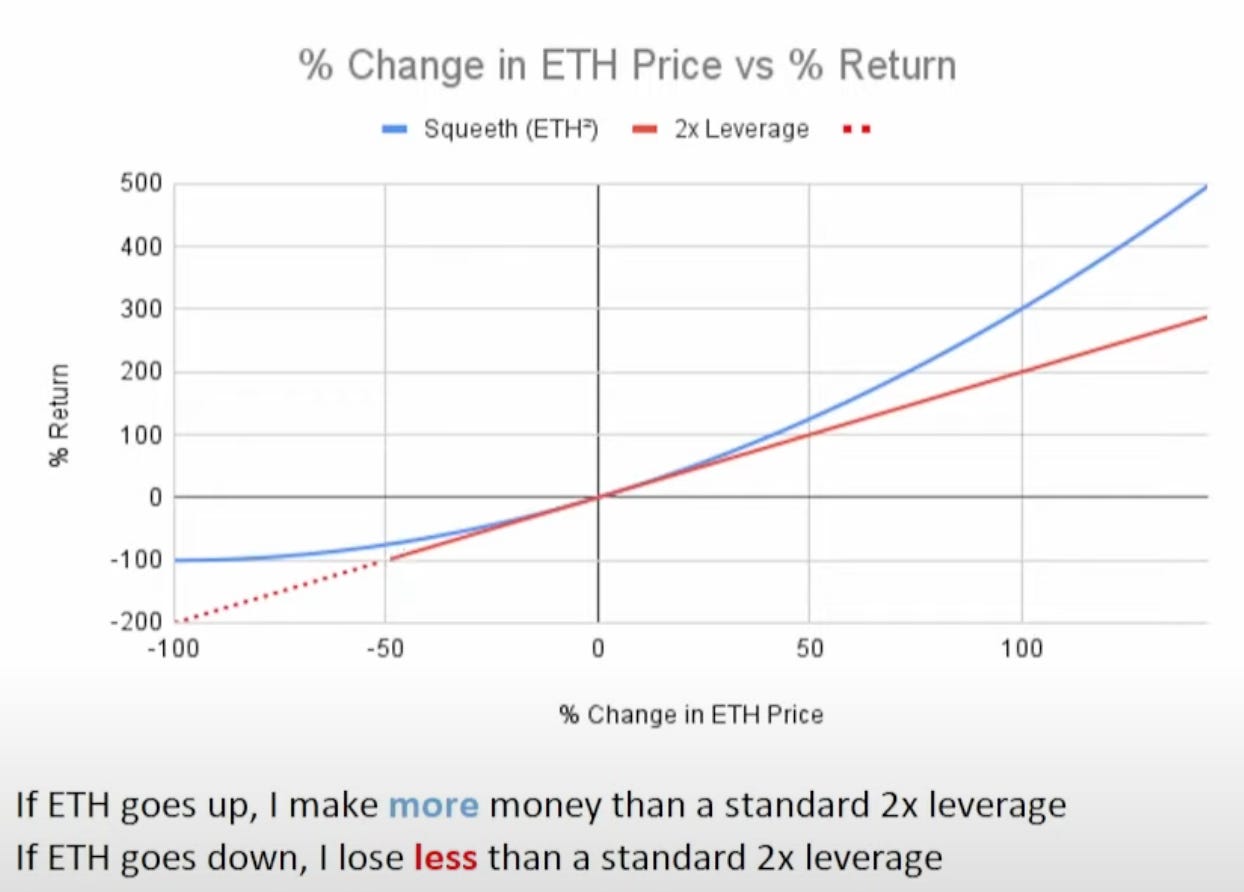

Here’s a visual diagram to describe the asymmetrical payoff.

To illustrate in numbers,

A normal return of an asset will be (1 + r) where r is the return.

Meanwhile, a power perpetual return will be (1 + r)² = r² + 2r + 1

Assuming ETH goes up by 20%,

Power perpetual will return (1 + 0.2)² = 1.44 or (+44%)

Now let’s say ETH goes down by 20%,

Power perpetual will return (1 - 0.2)² = 0.64 or (-36%)

Contrast this with a 2x leverage where up gives you 40% and down gives you -40%. Here you can see power perpetual gives you more return when prices go up and reduces your losses when the price goes down.

That’s the benefit of a convex exponential payoff compared to a traditional linear curve. The product is already available, and it is called Long Squeeth, created by Opyn.

This is the first power perpetual product not only in the history of DeFi but also TradFi.

Then you might ask, what’s the catch for this? I mean, obviously, everybody wants this power perpetual payoff where you win more if the price goes up and lose less when the price goes down.

The catch is longs need to pay a high funding rate for this convexity exposure.

2. How does it work?

On the opposite side of the long squeeth are the shorts. Shorts deposit their ETH as collateral, mint squeeth, sell them to long, receive a funding rate for it, and risk being liquidated.

The price of squeeth will be based on the variables,

ETH price movements (squared)

Funding rate

Implied volatility (squared)

The next question is how is funding rate determined.

Before we begin, there are two prices: the “mark price” and the “index price.” Just like a traditional perpetual instrument, the mark is the market trading price, and the index is what the derivative is tracking.

In this case, the index price of a squeeth will track ETH². If ETH is $1,000, the index price will be $1,000,000.

The mark price is based on basic demand and supply, alongside arbitrage bots to take advantage of any inefficiencies. Price is high when there are more buyers than sellers, and vice versa.

Suppose the mark price is exactly the same as the index price, let’s see what will happen.

A trader can go long power perp + short 2x leverage to get this payoff.

long payoff: r² + 2r + 1

short payoff: -(1 + 2r)

Combining both will give you a risk-free profit of r². Hence it is unlikely that the mark price will be the same as the index price as the arbitrage bots will definitely come in.

What about if the mark price is less than the index price? This is even more unlikely as this is saying that there is more supply of shorts than demand for longs. And longs are getting paid funding fees to hold an asymmetrical payoff position.

Hence, the mark price will trade higher than the index price most of the time due to the convexity premium.

The funding rate is used to incentivize the ratio of longs and shorts so that mark trades close to the index.

If the mark is trading at a much higher price than the index, it means demand for long squeeth is higher than the supply of short squeeth. At this point, funding yields will be elevated, and shorts will be incentivized to mint and sell squeeth.

Vice versa, if the mark is trading close to the index price, it means demand for buyers is low, and the supply of sellers is high. At this point, funding yields will be lower, longs will jump in, and shorts might buy back to repay their loans.

In short, the funding rate is the premium of mark over index, and it’s a reflection of the market’s expected future volatility.

High funding rate = high demand of buyers = higher expectation of volatility

3. Best Time go Long/Short Squeeth

So when is the good time to go long squeeth? The answer is simple: if you think the market is going to pump in the short term.

Time is not your friend for long squeeth. It is not something that you HODL long-term and forgets about it because you pay a funding fee continuously to the shorts for holding your position. And the funding fees are much higher than traditional perps.

The longer the market doesn’t pump and react to your thesis, the lower your returns will be as it is eaten up by the funding fees that accumulate over time.

On the other side of the coin, when should you sell squeeth? The answer is if you think the markets are overpricing volatility, but you are thinking it will trade sideways. Basically, you are shorting volatility.

How does it work?

When volatility is high, funding fees will be high. That is the best time for shorts to make money if you are right.

So you sell squeeth at the top and collect fees from longs. If the realized volatility is less than the implied volatility, the price of squeeth will drop, and you can buy back to repay your debt, withdraw your collateral and earn from the spread + the yields during that period.

As long as the cumulative funding fees received from shorts > daily volatility of ETH price movements (squared), it will be profitable to short squeeth. Time is your friend here, the longer the markets stay boring, the more money you make.

The risk for shorts is if your thesis is wrong. That means the markets turned out to be volatile as expected and the realized volatility is more than the implied volatility. In such cases, your deposited ETH has a chance of being liquidated.

4. Implied Volatility

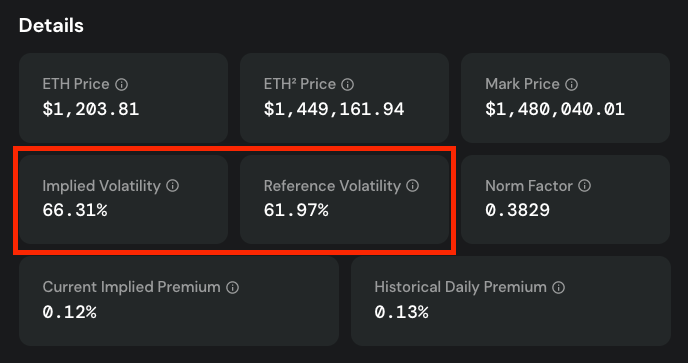

Next, how do you tell if the price of Squeeth is cheap or expensive in the market?

Generally, when volatility is high, the price of squeeth is high, and when volatility is low, the price of squeeth is low.

Ideally, you want to sell Squeeth when it is high and buy when it is low.

One way is to compare the Squeeth IV against the reference volatility which is derived from Deribit Exchange options. If it is lower than the reference, squeeth is selling at a discount, and if it is higher than the reference, squeeth is selling at a premium.

Zooming in on Deribit’s implied volatility index (DVOL), you can use it to gauge the 30-day forward-looking annualized expectation of volatility. If the DVOL is 70, it can be interpreted as the daily price movement of ETH would fluctuate between +/- 70/sqrt(365) or 3.66% in the next 30 days.

Alternatively, you could look back at the historical annualized Vol on Opyn’s trade page to see if it is high or low. For example from the period of Aug to Dec, it would be a good time to sell squeeth when volatility is at 130% - 140% and buy when it is around 50%. Though the past is not predictive of future performance, it tells you whether the current price is cheap or expensive based on historical performance.

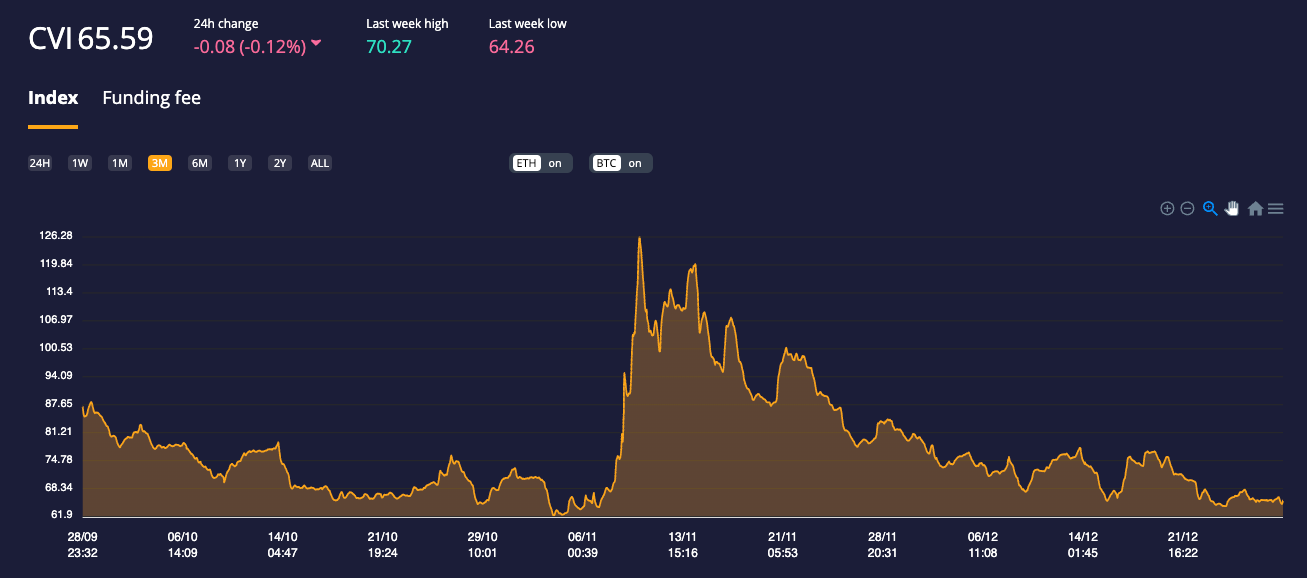

Finally, COTI network has also created a decentralized VIX for crypto (CVI), jointly developed by Dan Galai, the original creator of VIX for TradFi. The CVI tracks the 30-day implied volatility of bitcoin and Ethereum and ranges between 0 to 200.

0 - 85 = Low volatility

85 - 105 = Medium volatility

105 - 200 = High volatility

The CVI can be used as another market reference point for implied volatility apart from the reference volatility on Opyn.

5. Navigating Opyn’s Platform

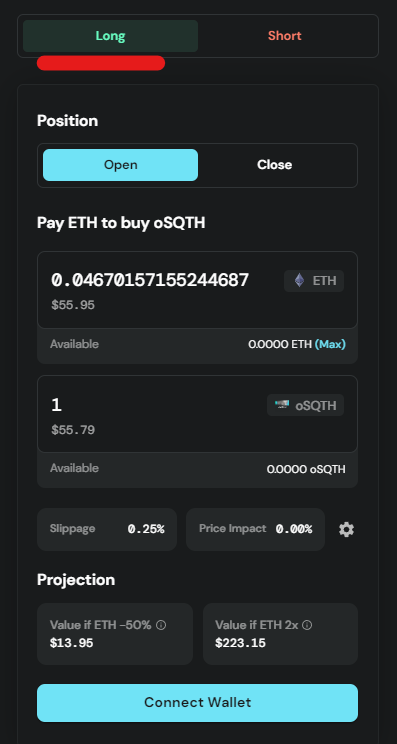

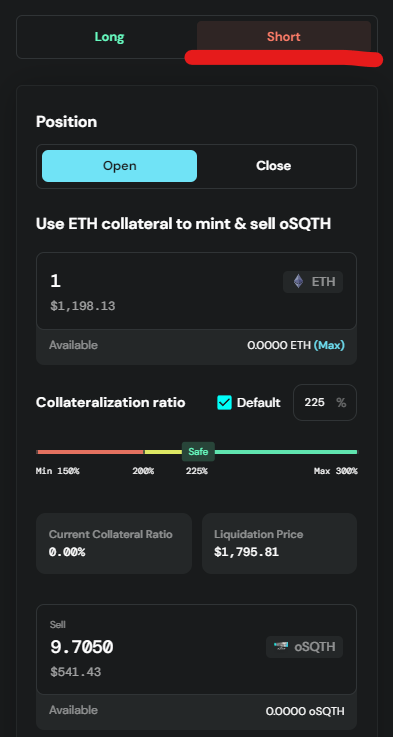

Here is a quick run-through on the Opyn’s platform and how to long or short.

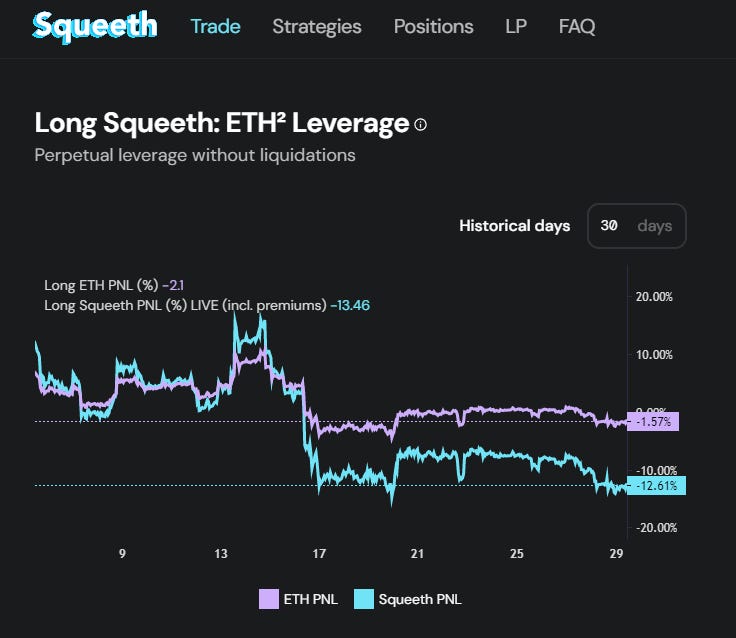

Here you can see that Squeeth’s P&L for ETH has not been doing so well for the past 30 days. Very simply because there was no action and the markets are slow. Long squeeth only wins if the market pumps hard and fast, which is not the case recently.

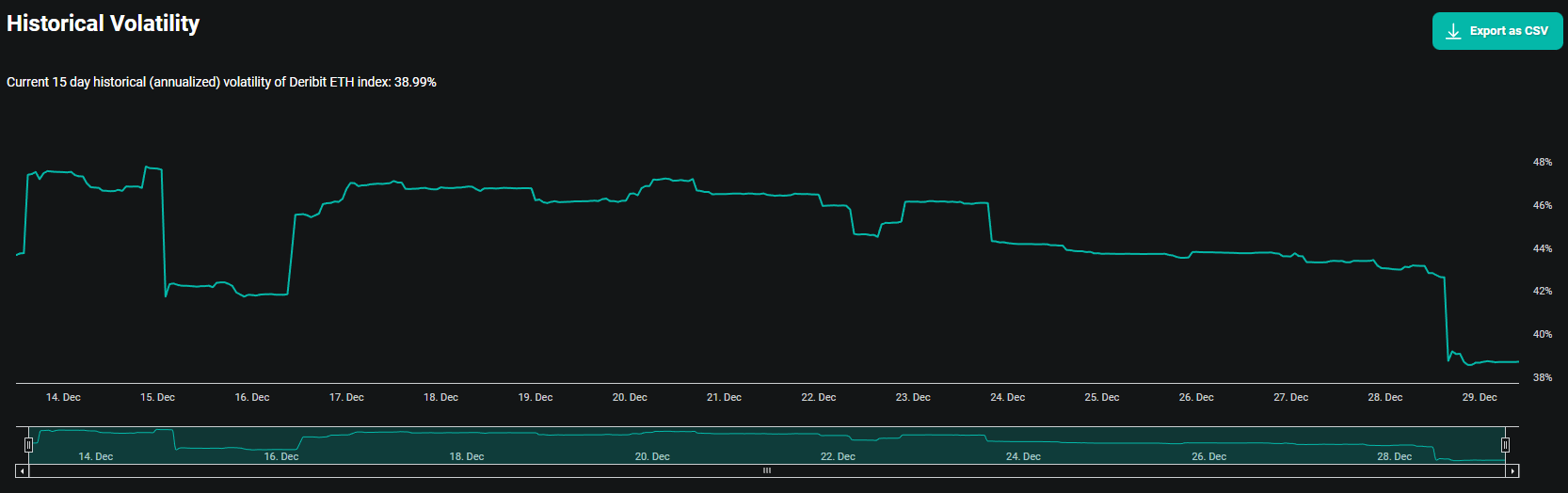

Historical volatility on Deribit also confirms that ETH annualized volatility is only about 39%. Pretty flattish for the month.

But suppose you think markets are going to pump soon, you could click long and select how much exposure you want to have. It is pretty straightforward. The nice thing about Opyn is they also show how much you could make and lose if the price 2x or dumps -50%.

Shorts are more tricky as you have to watch for your liquidation price. The safe collateralization ratio is 225% so if you deposit 1 ETH, your exposure is only about half. And if ETH falls to the liquidation price, you could lose a share of your collateral.

By minting oSQTH, it is a debt owed by the short that can be repaid anytime you want. Assuming all things equal, the price of oSQTH would gradually go up from the funding fee received from longs. But other variables such as ETH price and volatility also dictate whether oSQTH goes up or down.

The ideal case for shorts would be to sell oSQTH at the top and buy oSQTH at the bottom to close their position and withdraw their deposited ETH collateral.

That’s pretty much the basics of what Squeeth is and how to long or short.

6. Summary

To sum up, power perpetual,

Allows you to earn more when the price is up and lose less when the price is down

Cost of holding this asymmetrical convexity exposure is paying a funding fee

Funding fee is the premium of the mark over the index

The funding fee is a reflection of implied market volatility

More buyers > more volatility expected > higher funding fee

The opposite side of the trade is short squeeth

Shorts deposit ETH as collateral, mint squeeth to longs in return for funding fees

Returns are based on ETH price movement, funding rate, and implied volatility

Long squeeth if you think ETH is going to pump and squeeth is cheap

Short squeeth if you think volatility is overpriced and squeeth is expensive

Implied volatility on squeeth can be referenced against Deribit or historically

The introduction of power perpetual has unlocked novel use cases and opportunities in DeFi. Understanding the mechanism behind power perpetual lays the foundation for wrapping your head around other exotic strategies in the power perp ecosystem. More articles around power perp to come soon.

Image credit reference:

https://medium.com/opyn/how-to-think-about-squeeth-returns-8646fd57f559