Overview of ETH Liquid Staking Landscape

ETH Staking Yields

1. Introduction to Liquid Staking

What is liquid staking?

After The Merge event, ETH transitioned from the Proof-of-Work (PoW) to the Proof-of-Stake (PoS) economy.

In the new PoS chain, staking ETH allows you to earn a yield of between 5-10%, paid natively in ETH.

The yields come from inflationary emissions (part of ETH tokenomics design) for

Validating and proposing blocks at the consensus layer, plus

Users’ tips and fees at the execution layer.

This was previously unavailable to the regular user as rewards only go to the specialized miners in the PoW economy. But now, you can stake your ETH with any node validators in a single click and earn a portion of those rewards.

As such, ETH can be considered a perpetual bond that pays a low-risk yield with no expiry date.

However, when you deposit your ETH with a validator to earn staking rewards, it is typically locked up, and that’s capital inefficient.

What if it could be unlocked, and you use your deposited staked ETH as collateral to borrow stablecoins and earn additional yields elsewhere?

That’s the value proposition of Liquid Staking; it unlocks the liquidity of your staked assets and makes them liquid & composable so that you may generate additional opportunities on top of the regular staking yields you earn daily.

To unlock the liquidity of staked assets, a % cut on the rewards is charged and paid to the liquid staking protocols, and that’s how they make money.

In short, liquid staking unlocks the liquidity of staked assets, and you pay a fee for it, which could be thought of as the premium for liquidity.

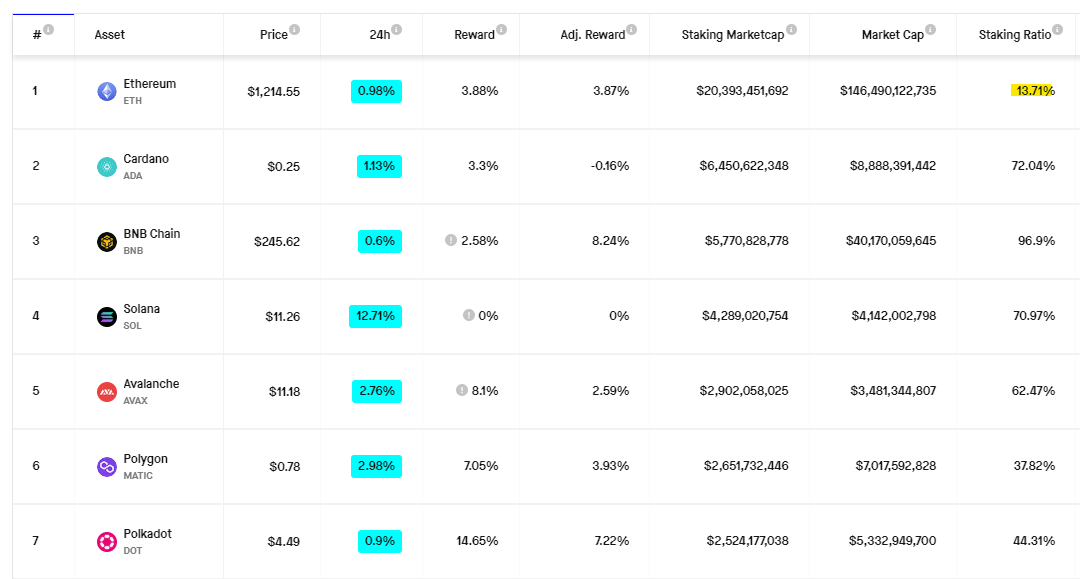

Based on the data from StakingRewards, only about 13.7% of the circulating ETH supply is currently being staked.

So few people are staking ETH right now because once you stake it, it can’t be withdrawn until the next upgrade, called the Shanghai hard fork. (ETA March 2023, but could be pushed back)

This, of course, made people wary and hesitant to stake as many unknown risks could happen in between, both on the Ethereum layer as well as on the protocol layer. You don’t know when you can withdraw back your ETH.

Not to mention the risk-averse, “flight-to-safety” mentality in the bearish market environment. Only a few would be willing to hold illiquid assets.

However, that will soon change after the Shanghai upgrade, enabling the staking withdrawal feature for anyone.

2. Who are the Players in the Game?

This will have enormous implications for all the liquid staking entities, including Coinbase.

More people will be comfortable staking liquid assets, and as more people begin staking their ETH, fees across the liquid staking sector would skyrocket.

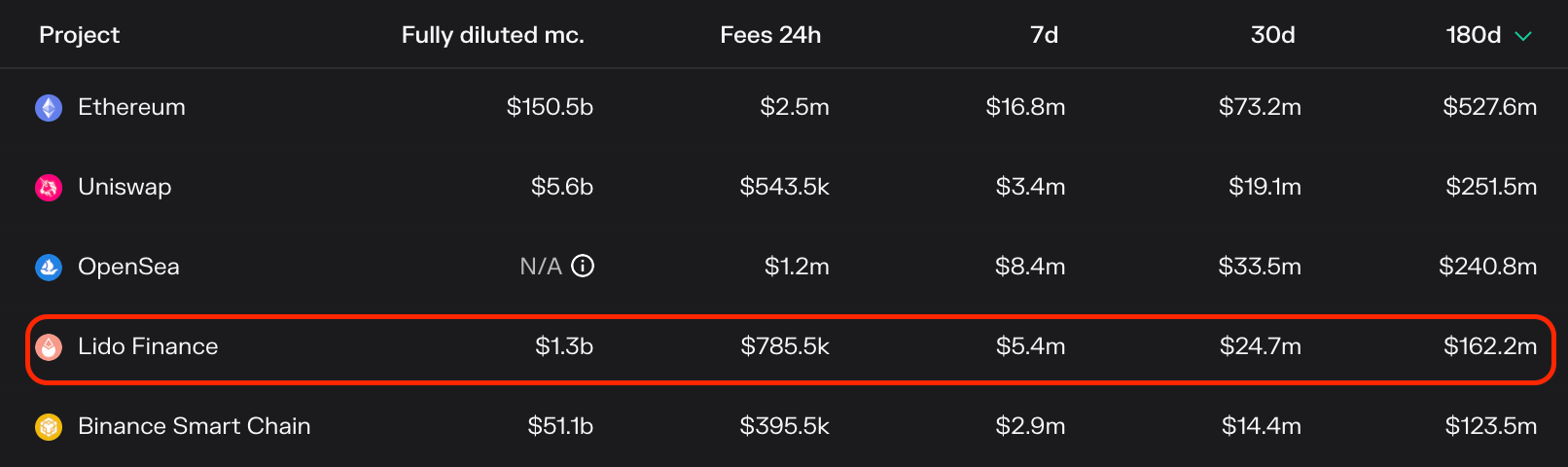

To put things into context, Lido Finance, the market leader in this sector, currently generates about $162m in fees over the past six months, or about 900k daily on average.

It is one of the top 5 projects in the crypto universe, three places behind Ethereum.

As a rising tide lifts all boats, all the tokens relating to liquid staking have been pumping over the past week, attempting to price in the event catalyst.

But a period where everyone is shilling hard is typically not the best entry point for an investment to buy in. It’s a typical “sell the news” event kind of price movement.

The other train of thought is that once staking withdrawals are enabled, most people that have locked up their ETH previously would be quick to sell, especially in this period when liquidity is important.

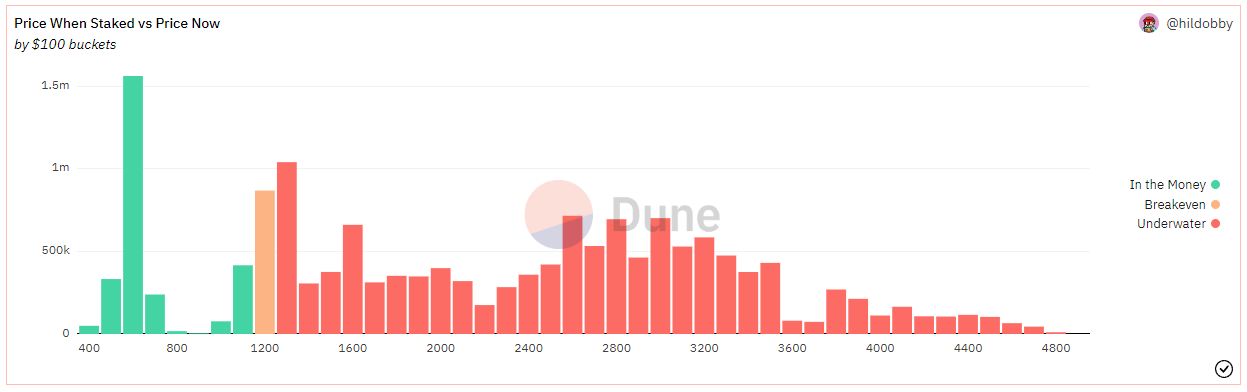

About 77% of those who staked ETH were done months ago when ETH was trading at a much higher price. So although the point at which they staked ETH is not necessarily their entry-buy price, it gives us a good sense of how many people are at a loss.

Also, the counter-argument is that those who staked ETH are typically long-term investors, and they are unlikely to dump over short-term speculations. Let’s see.

3. Lido Finance

Lido is the number #1 player in the liquid staking sector.

How it works is you deposit ETH, and get back stETH which is Lido’s version of “staked ETH.”

Now you can use this stETH to do other stuff like a deposit as collateral to borrow or LP on Curve.

While doing all these, your stETH will continue accruing rewards, of which 10% goes to Lido. (50% to Node operators, 50% to Treasury)

Lido has another token called the wrapped stETH or wstETH.

The difference is that stETH is a rebasing token, meaning its balance change over time as rewards accrue, but wstETH balance stays the same while the value increases.

The reason why there is another "wrapped” stETH is because DeFi protocols like MakerDAO, Sushiswap, and Uniswap don’t work well with rebasing tokens where the quantity balance should be constant.

Using wrapped stETH solves this problem as the quantity will be the same in the pool, but its value will increase over time to reflect the accrued staking rewards.

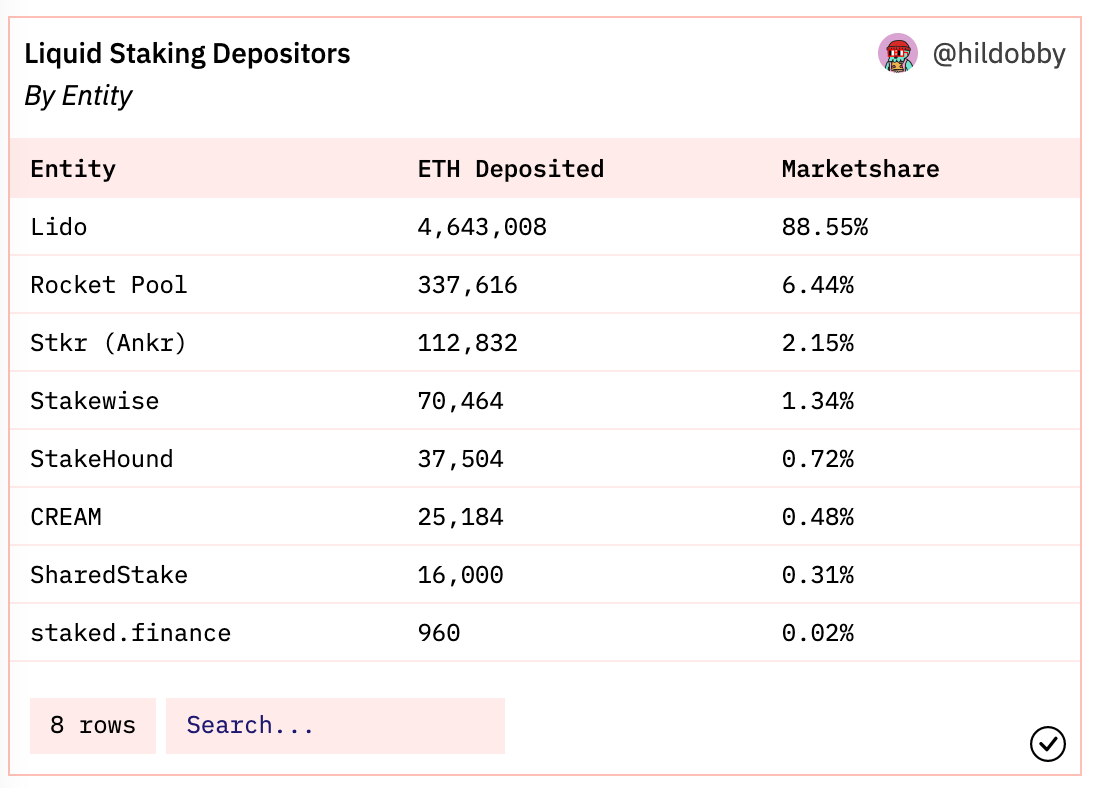

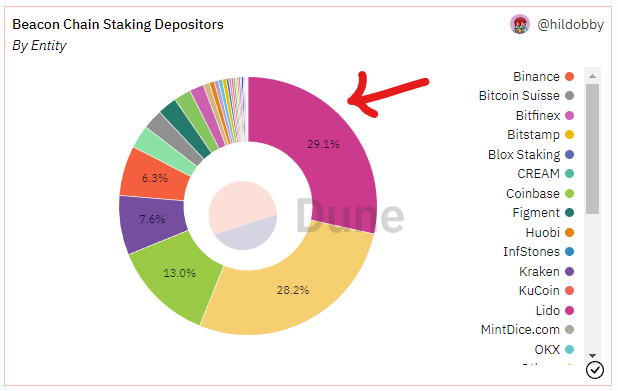

Regarding market share, Lido is a centralized monopoly today, controlling slightly less than 1/3 of the ETH supply with 88% market share amongst other projects. 33.33% is the point where the market gets unnerving.

That is a big problem as it creates a central point of attack, cartelization, abuse of governance power, collusion for block space, block-ordering, transaction censorship, and MEVs, to name a few. This poses a potential threat and systematic risk for Ethereum.

Hence, the community is focusing on the decentralization & distribution of staking ETH to protect the network from any of these risks.

Apart from the centralization issues, Lido is also multi-chain on Polygon, L2s, Kusama, Polkadot, Solana, etc.

While it’s good to have an extensive reach and market across other ecosystems, there is also criticism around Lido’s commitment to Ethereum and unnecessary incentives (currently 2.8m to 3.1m~) for liquidity pools that are low in volume. It is roughly about 3.6%~ of annual emissions for incentives based on the past 2 months.

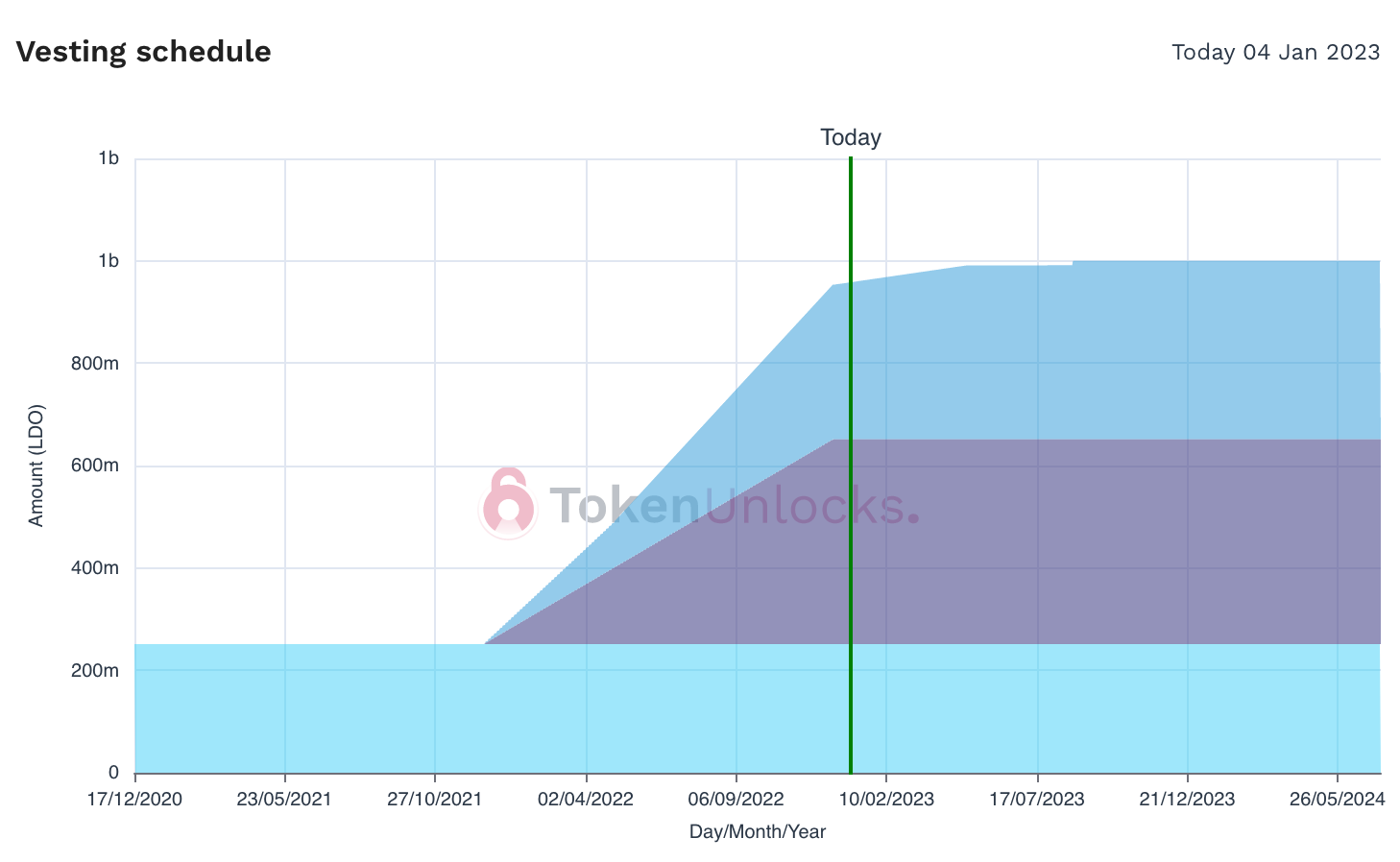

Nevertheless, the good news for Lido is that it just finished its biggest investor unlock (the steepest part of the vesting schedule has been released). About 83% of the tokens are already in circulation, and the supply inflow has slowed significantly.

Lido’s biggest competitor is Rocket Pool, the 2nd largest liquid staking protocol.

4. Rocket Pool

Rocket Pool prides itself on prioritizing decentralization, a plaguing problem on Ethereum liquid staking landscape right now.

Running a node operator on the Rocket pool is permissionless.

Anyone can run a node, unlike Lido, which has a registry controlled by LDO token holders, and only they can add new operators.

The capital requirement for setting up a node is much lesser, only 16 ETH, compared to the Ethereum requirement of 32 ETH. The other 16 ETH is paired up from a deposit pool of individual stakers like you and me.

The validator will receive the full yield from their 16 ETH + a 15% commission rate on the 16 ETH they will stake on behalf of the pool of regular retail stakers.

Unlike Lido, which takes a 10% cut of the rewards (5% to treasury & 5% to node operators), Rocket Pool takes a 15% cut and gives 100% to node operators directly.

Like Lido, you stake ETH, receive back rETH, Rocket Pool’s version of staked ETH, and your rETH will automatically accrue rewards like wstETH.

The upcoming LEB8 proposal plans to lower further the capital requirements for nodes from 16 ETH to 8 ETH to lower the barrier of entry, increase decentralization, and improve capital efficiency.

Since anyone can join as a node, the safeguard for Rocket Pool protocol is to introduce a bonding system. Validators must deposit a minimum of 10% up to 150% on their 16 ETH, in RPL tokens, as additional insurance in case of a slashing or penalty.

The node operators earn additional RPL tokens as incentives on their collateral deposit. Currently, the RPL inflation rate is 5%, of which 70% is directed towards this means. The other 15% goes to oracle DAO and 15% to protocol treasury.

From a protocol’s perspective, Rocket Pool doesn’t take a fee cut on the rewards but instead earns from its own RPL token emissions, contrasting with Lido’s 5% take rate.

Also, while RPL has an added utility for insurance, it could be a burden for nodes as they are required to buy RPL tokens for their collateral, manage, and top up additional RPL tokens if the price fluctuates.

Scaling is also challenging as you have to balance the supply and demand of the mini pools from node operators and the deposit pools from the public. This is currently done by putting a limit cap and arbitrating premiums/discounts for the rETH by node operators.

Nevertheless, if there’s a move toward alleviating Lido’s centralization risk, Rocket Pool will likely be the primary beneficiary for the spillovers, amongst other liquid staking projects.

5. Stakewise

The project that pumped the hardest is Stakewise, the smaller-cap plays.

What makes Stakewise attractive is its tokenomics design. It is the only one proposing to pay out 80%-100% of fees earned from the DAO back to the SWISE token holders, unlike Lido, which is like Uniswap, and Rocket Pool which doesn’t earn protocol fees.

Stakewise also has a “hope catalyst” element as it is launching v3 soon in Q1.

The core of v3 is that it allows anyone to set up node operators known as “vaults” permissionlessly.

Each vault will have its own “vault token” and a scoring system based on effectiveness, decentralization, client diversity, etc.

As a user, you could specifically choose which node operators (vault) you are comfortable staking your ETH with.

Upon deposit, you would receive the “vault” token of your choice, representing the ETH staked in their respective vault.

You could imagine a scenario where different vaults will give different yields based on the performance of each vault.

For those who want to unlock the liquidity of the staked ETH, you could go one step further to deposit vault tokens as collateral and mint osETH, Stakewise’s version of staked ETH.

osETH will be overcollateralized in the event of slashing penalties.

Alternatively, you could buy osETH directly from the secondary market if you want a diversified backing of vaults, as all osETH minted are overcollateralized.

The main reason one would want to mint osETH is if they are vault operators and they want to control or isolate their risk exposure to their internal operations.

Stakewise is also working on a new tokenomics design allowing the SWISE tokens to be used as bonding insurance for vaults.

If the vaults are slashed, the SWISE bonded would be akin to the junior tranche, where it is automatically sold to compensate the minters of osETH from that vault.

In return, StakewiseDAO will distribute its revenue earned from osETH minting fees back to the bond stakers, with a limit cap based on the vault’s market share.

In this way, the SWISE token has more utility and value accrual, vaults are safer and insured, osETH adds buffer on top of over-collateralization, and more people will have confidence over the vaults and osETH and the flywheel kicks in.

Stakewise has a more interesting tokenomics model, stronger value accrual, and a new design mechanism. However, it’s still largely untested, there’s a technical migration to a new infrastructure, and it’s in the middle of a steep vesting schedule.

6. Conclusion

Here’s a quick overview of the adoption stats and valuations across the 3 liquid staking protocols as of writing. Despite Lido’s strong adoption stats and dominance in the sector, markets still favor the challengers and underdogs with the hope of a greater upside, decentralization premium, scalability factors, and token value accrual.

From a user perspective, the different versions of staked ETH from different protocols would have slight variances in APR yields, depending on the commission rate and node operators’ effectiveness.

But APR should not be the only consideration, as other factors like node decentralization, collateral buffers, protocol risks, and insurance are equally important things to look into.

In the next 3 months, it will be interesting to see the market’s reaction toward Ethereum’s next big milestone, the Shanghai upgrade, and the power dynamics when liquid staking withdrawals are enabled.